Loading categories...

The African Critical Mineral Engine

Geologic arbitrage, commercial flows & geopolitical choke points — interactive research infographics (A++ 2026 Edition)

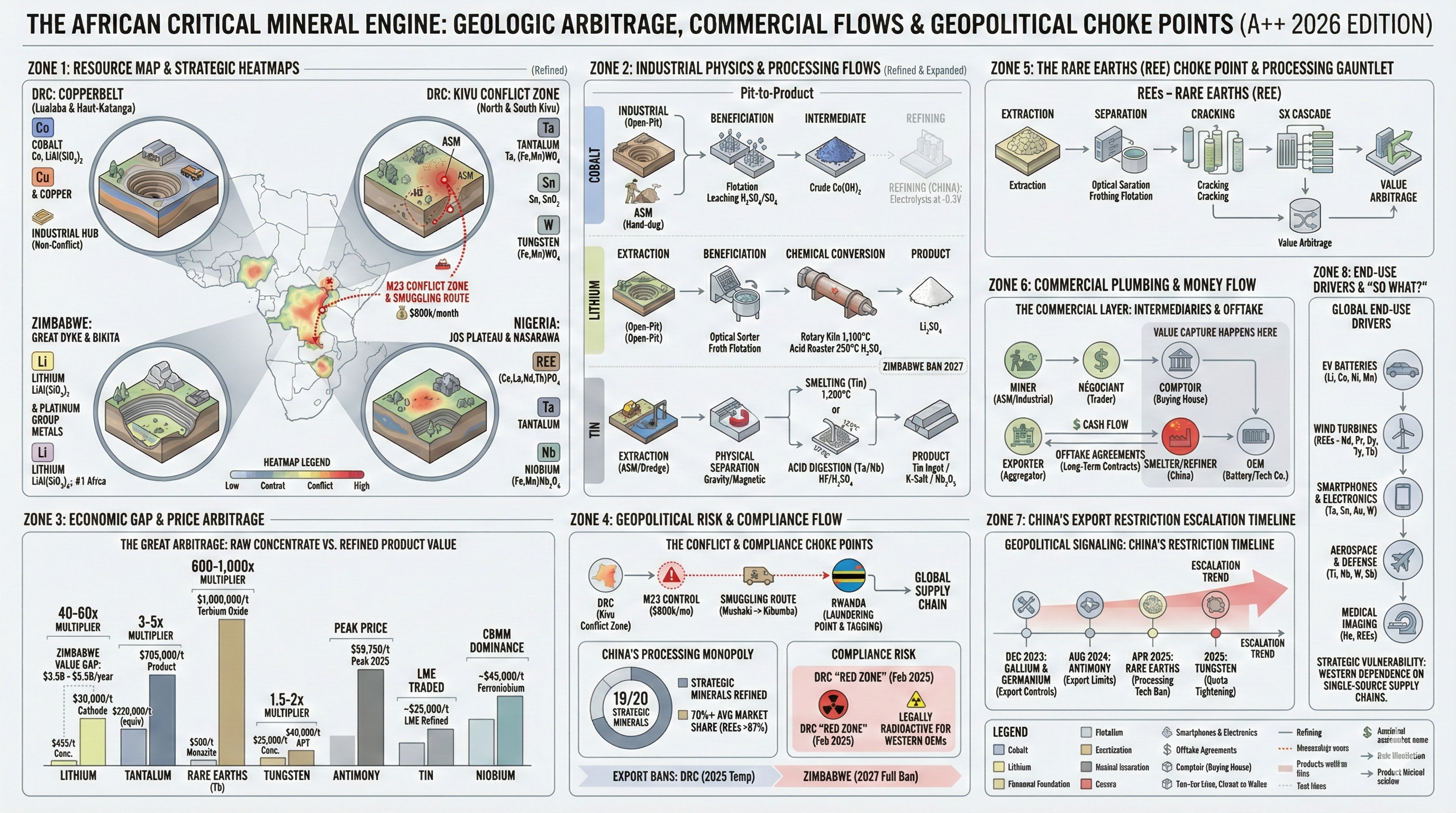

Resource Map & Strategic Heatmaps

Key producing nations, mineral deposits, conflict zones, and resource concentration by country.

Strategic Mineral Heat Map

Production share + reserves intensity by mineral and country. Higher = more concentrated supply risk.

Industrial Processing Flows

Pit-to-product value chains showing exactly how raw African minerals become refined components. Value capture is overwhelmingly outside Africa.

The Great Arbitrage

Raw concentrate vs refined product value. Africa captures the low end; China & the West capture the multiplied value.

Note: multipliers compare raw product to refined product on a per-tonne basis; for contained-metal equivalents, adjust for grade and payability. Data as of Q4 2024 / early 2025 unless otherwise noted.

Geopolitical Risk & Compliance

Conflict zones, smuggling routes, export bans, and compliance choke points across African mineral supply chains.

China's Processing Monopoly

19 of 20 strategic minerals processed in China. Escalating export controls weaponize supply chains.

Export Restriction Escalation Timeline

Each wave targets minerals where China has dominant processing capacity — even when raw materials originate elsewhere.

End-Use Drivers — “So What?”

Global demand sectors consuming critical minerals. Each sector creates structural demand growth independent of commodity cycles.

Market Data — Live Prices

Real-time prices for critical & strategic mineral equities and ETFs. Click any row to expand daily/weekly/monthly charts.

| Ticker | Name | Last | 1D % | Trend |

|---|